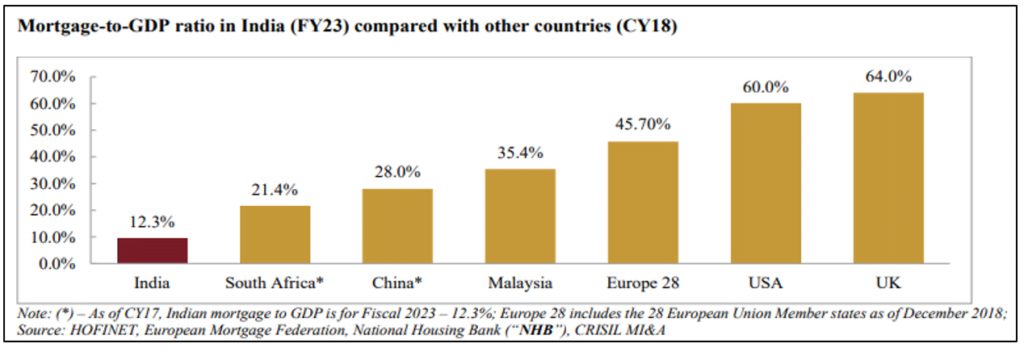

CRISIL further adds that rural areas, which accounted for 47% of GDP, received only 8% of total banking credit, indicating a large market opportunity for banks and NBFCs to lend in these areas.

With the government’s increasing focus on financial inclusion, rising financial awareness, and increasing smartphone and internet penetration, the delivery of credit services is expected to increase.

Compared to overall housing loans, which increased by 14% between Fiscals 2018 and 2023, the growth in the low-income housing category has remained muted, with the segment experiencing a CAGR of 3% after expanding between Fiscals 2015 and 2018. The COVID-19 epidemic, a slowdown in economic activity, and financial difficulties brought on by the NBFC crisis are the leading causes. However, the situation has improved, and the low-income home loan market is predicted to rise at an 8-10% CAGR between FY 23 and FY 26.

There is a shift towards a nuclear family structure from the erstwhile joint family structure, which is increasing the need for housing in most parts of our country.

Beyond this, the broader reason for the growth of credit/housing, especially in Tier 2 to Tier 7 cities in India, is mainly driven by rapid urbanization, economic development, rising disposable incomes, and Favorable demographics. Government initiatives promoting financial inclusion, infrastructure developments, and expanding banking networks have facilitated easier access to credit. Increasing aspirations for better living standards and educational opportunities also spur loan demand. Cultural changes and improved access to information contribute to the growing consumer base seeking various forms of credit, from personal loans to housing finance. These factors collectively support the expansion of credit facilities in smaller cities and towns across India.

As per the RBI Report of the Committee on the Development of Housing Finance Securitization Market published in September 2019, the housing shortage is also largely in the EWS and LIG segments (Economically weaker section/Low-income group), with 45 million houses in the EWS segment and 50 million houses in the LIG segment, which together account for 95% of the estimated housing shortage in India.

Hence, the government of India has specially come up with PM Awas Yojna to provide affordable housing for the urban and rural poor in the country. Pradhan Mantri Awas Yojana (PMAY) is a flagship housing scheme launched by the Indian government to provide affordable housing to urban and rural poor by 2022 (extended till Dec 2024). It aims to promote affordable housing through financial assistance, subsidies, and home construction and renovation incentives. The scheme targets economically weaker sections (EWS), low-income groups (LIG), and middle-income groups (MIG) across India.

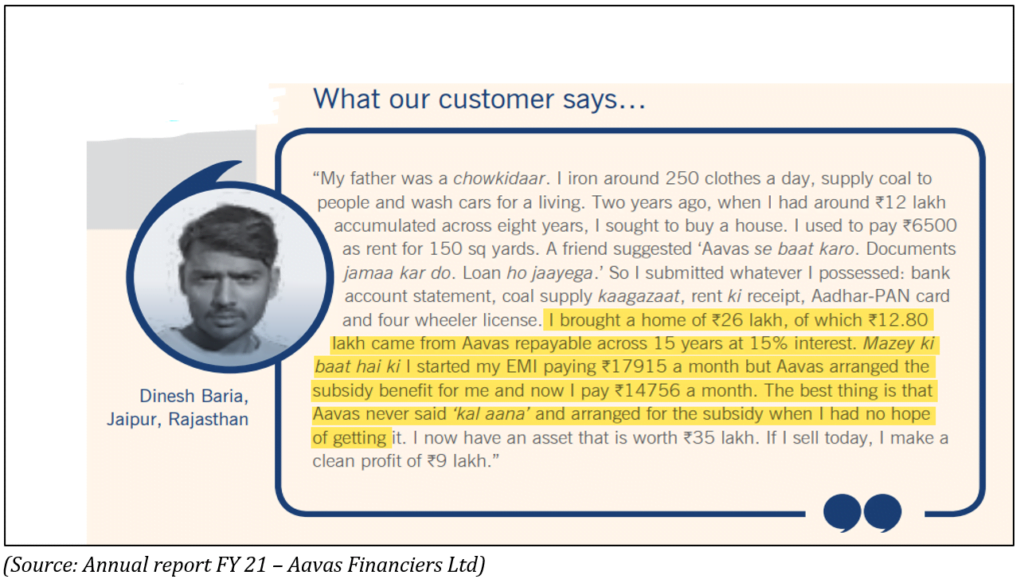

So companies like Aavas financiers benefit from it, and small housing finance companies contribute significantly to the growth of tier 2 and 3 cities by providing accessible financing options tailored to local needs. They bridge the gap in housing finance, catering to underserved segments with flexible loan terms and personalized customer service. By facilitating easier access to housing loans, they stimulate real estate development, boost home ownership rates, and contribute to overall economic expansion in these cities.