The S&P 500 is up nearly 30% for the year. With markets rising steadily all year, it is unsurprising to witness investors lulled into an elevated sense of complacency.Stocks, Bitcoin, leveraged investments, and meme stocks are all surging higher, which is certainly reminiscent of the“madness” we witnessed following the Covid lockdowns.

In this article, we examine multiple indicators related to the US economy that don’t bode well for the US economy. Some of these factors can individually or cumulatively trigger a recession in the US.

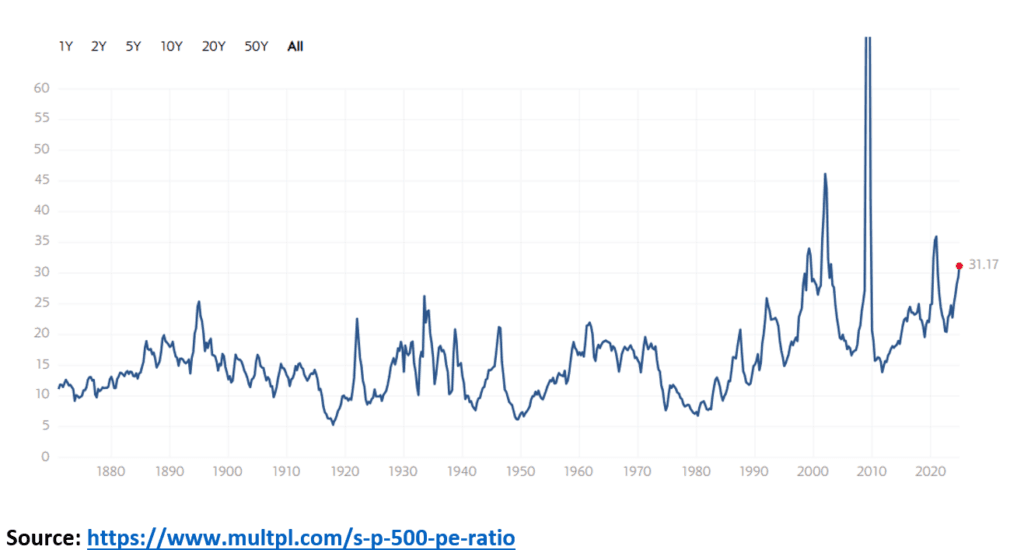

S&P 500 P/E Ratio & High Concentration of Top 10 Stocks

As of Dec 6, 2024, the S&P 500 index trades at a P/E of 31.2x. As you can see, the S&P 500 has crossed 25x only a few times, the majority leading to massive stock market crashes, including the dot com bubble, the 2008 financial crisis, and COVID-19.

It is also disturbing that as of December 2024, the concentration of Top 10 stocks in the S&P 500 is at its highest level in 30 years, with the top 10 stocks accounting for nearly ~35% of the index. This significant concentration indicates a few companies dominate the performance of the S&P 500, which raises concerns about market stability and the effects of this concentrated growth on overall market diversity. Also to be noted is that the ten largest stocks trade at a premium of about 32% to the S&P 500 index.

A reversal can be expected; hence, the S&P 500 index could underperform significantly for many years due to two main reasons: elevated valuations and market concentration.

Credit card delinquencies mount:

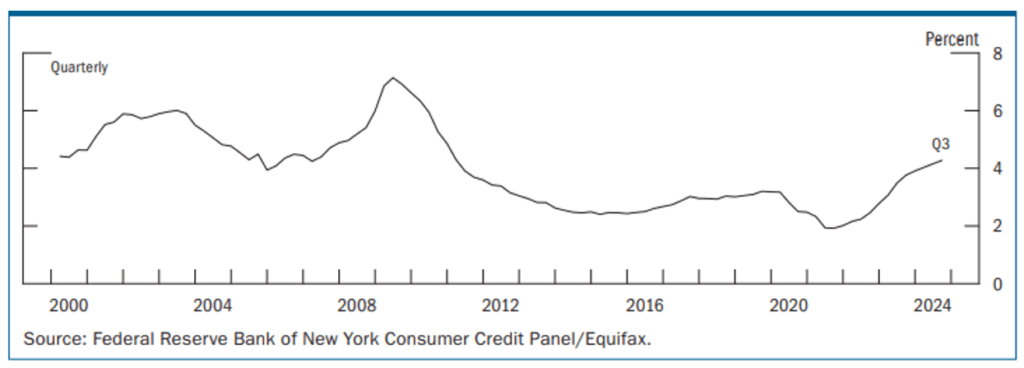

The Federal Reserve’s annual financial stability report reveals a significant increase in credit card delinquencies, which have surpassed 4% for the first time since 2010, primarily affecting nonprime borrowers. Concurrently, consumer credit card debt has risen by 6.7% to reach $1.3 trillion, outpacing historical growth rates and reflecting a concerning trend of riskier lending practices.

Inflation-adjusted credit card balances for subprime borrowers trended higher but below previous peaks as of the latest quarter, as shown in the above chart.

As shown in the chart above, credit card delinquencies rose further to somewhat above their pre-pandemic levels.

Sahm Rule Recession Indicator:

In August 2024, the Sahm rule recession indicator rose to 0.57%, which was above the recession indicator threshold.

The Sahm Rule serves as a crucial recession indicator. It signifies the onset of a recession when the unemployment rate rises by at least 0.50 percentage points from its 12-month low. This tool has effectively predicted every recession since 1970, providing policymakers with an essential threshold for intervention.

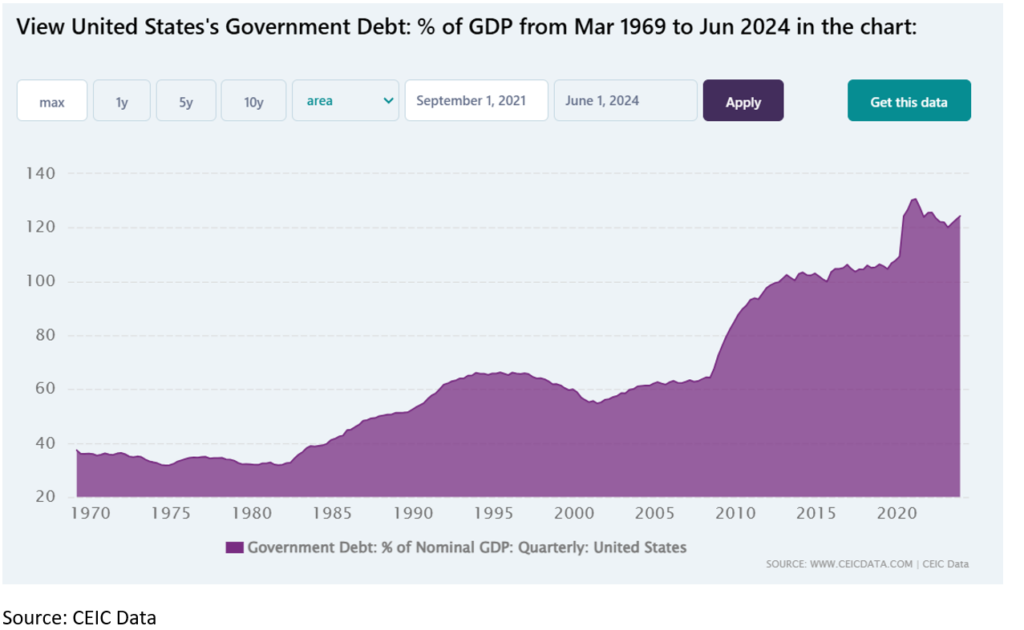

Debt to GDP Ratio:

As of December 2024, the debt-to-GDP ratio in the United States is projected to reach an all-time high of approximately 124.30%, reflecting ongoing increases in government debt. A high debt-to-GDP ratio can have a number of negatives on the US economy, including:

Reduced economic growth as most funds are used to repay interest on existing debt. In 2023, the US paid more than $1 trillion in interest on its public debt.

High debt levels can induce higher inflation in the economy. As the dollar loses its status as a reserve currency, the impact of higher debt levels on inflation can be much higher for the US economy as a whole.

10 Yr. Treasury Yield – 2 Yr. Treasury Yield:

The yield curve shows the difference in interest rates between short-term and long-term bonds. An inverted yield curve occurs when short-term interest rates are higher than long-term rates. This suggests that the near term is riskier than the long term. Yield curve inversions have preceded each of the last eight recessions. However, the timing can vary significantly, leading to the concept of a lag between inversion and the onset of a recession.

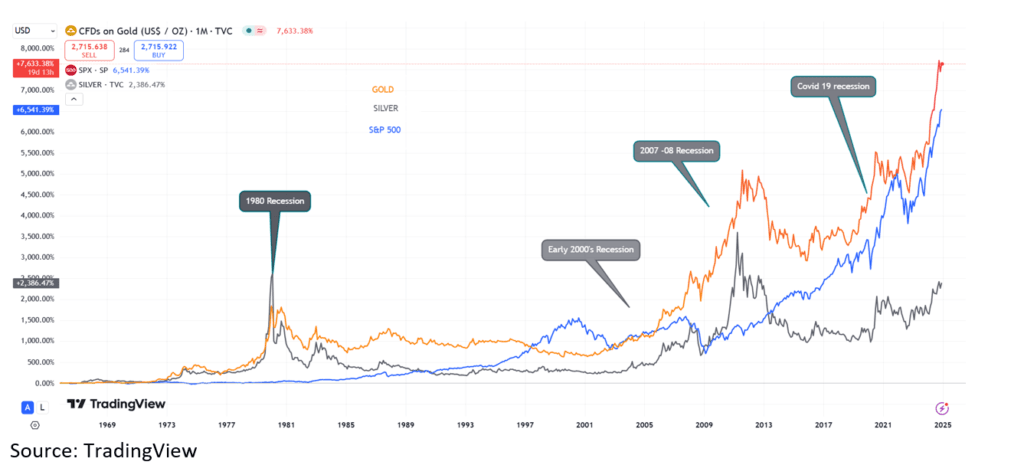

The potential impact of a US recession on Gold and Silver

Gold performance during periods of recession:

Great Depression: +69%

Stagflation (1973-1975): +100%

Early 2000s Recession: +60%

Great Recession (2008-09): +100%

COVID-19 Recession: +33%

Silver performance during periods of recession:

Great Depression: +50%

Stagflation (1973-1975): +300%

Early 2000s Recession: +25%

Great Recession (2008-09): +29%

COVID-19 Recession: +39%

These percentages illustrate how gold and silver have generally performed well during economic uncertainty, with notable increases during severe recessions and financial crises.

As of December 2024, Gold is trading close to its all-time highs. It is slightly contradictory that both Gold and the S&P 500 are trading at their all-time highs, given that gold is a hedge against equity markets and also the US dollar.

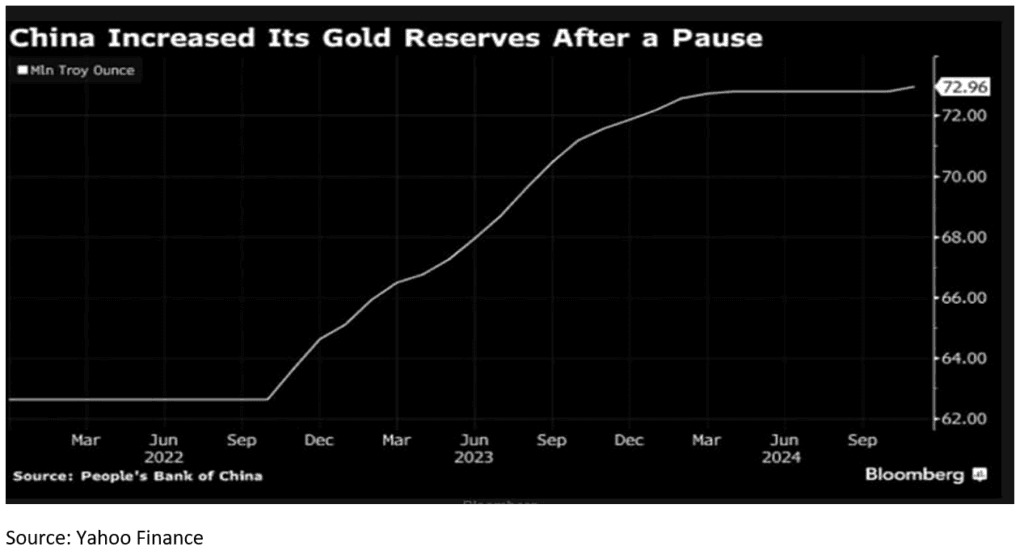

Notably, Central banks have been net buyers of gold since 2010, and in 2022 and 2023, they accounted for almost a quarter of annual gold demand. In 2024, central banks are still buying gold, and some notable buyers include:

The Reserve Bank of India (RBI) Has added gold every month so far in 2024, with net purchases totaling 37t

The People’s Bank of China (PBoC) Reported adding 27t to its gold reserves in Q1

The Central Bank of Turkey: Added 15t to official gold reserves in Q2

The National Bank of Poland (NBP): Was the largest purchaser in Q3 2024

It can’t be refuted that Gold and silver may also offer “a safe harbor” if geopolitical tensions worsen in 2025.

Silver has historically underperformed compared to gold in terms of long-term price appreciation. However, silver has experienced periods of significant gains, often outpacing gold during periods of economic weakness. Silver has both investment and industrial uses. This dual demand makes it attractive, as advancements in Green technology and 5G also continue to paint a positive picture for silver.

Silver has seen significant all-time highs, particularly in 1980 and 2011. In recent years, it has seen increased volatility and recovery. Due to its increased demand and global concerns, silver is inching upwards and has recently seen a breakout. We expect a long-term rally in silver, taking it to previous all-time highs as more clarity emerges on the US falling into a recession.

Conclusion

While it is difficult to say when exactly the US can enter a recession, data seems to suggest that things are not looking as great. There are multiple data points to be concerned about, and hence, these data points need careful tracking.

What is also important is that investors should take a very balanced approach to their portfolio and focus on value rather than chasing momentum. If and when there is more clarity on a potential recession in the US, both gold and silver are expected to do well; hence, taking some position can act as a hedge against equities.