Since September 2024, the Nifty 50 has been in a prolonged phase of consolidation, eventually turning into a meaningful correction. After a stellar rally from 7,600 (March 2020) to 26,200 (Aug 2024), a 3.5x surge in under 4 years, markets were bound to cool off.

This rally was driven by:

Strong FII inflows

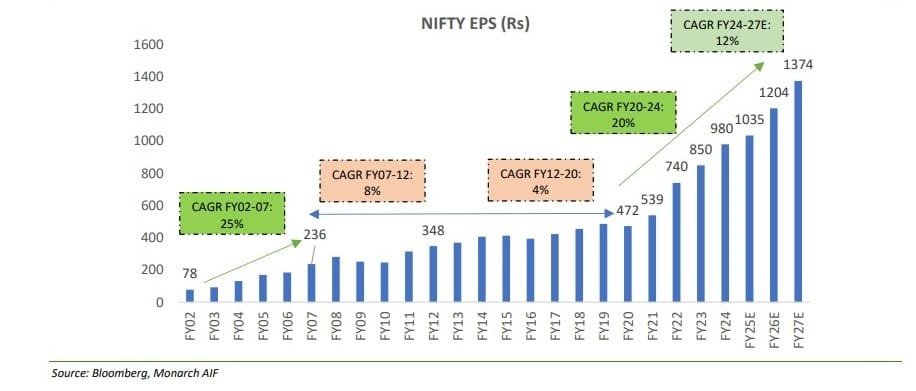

Consistent EPS growth (20%)

Liquidity-led valuation expansion

However, as valuations peaked, the market entered a mean-reversion phase, correcting nearly 23% to 21,200 levels.

1. Valuation premium became unsustainable

A major factor behind the sharper correction has been the relative valuation premium India commanded compared to other emerging markets. At the start of 2025, MSCI India was trading at nearly a 90% premium to MSCI Emerging Markets, significantly higher than its five-year average of around 75%. India’s forward P/E stood at approximately 22.3x versus the EM average of 11.7x. While India justified this premium due to its stable GDP growth of 6–7%, political stability, favorable demographics, and structural growth opportunities in manufacturing and technology, the premium became difficult to sustain once earnings growth began to moderate after a strong multi-year cycle.

2. Global Capital Rotation (FII Outflows)

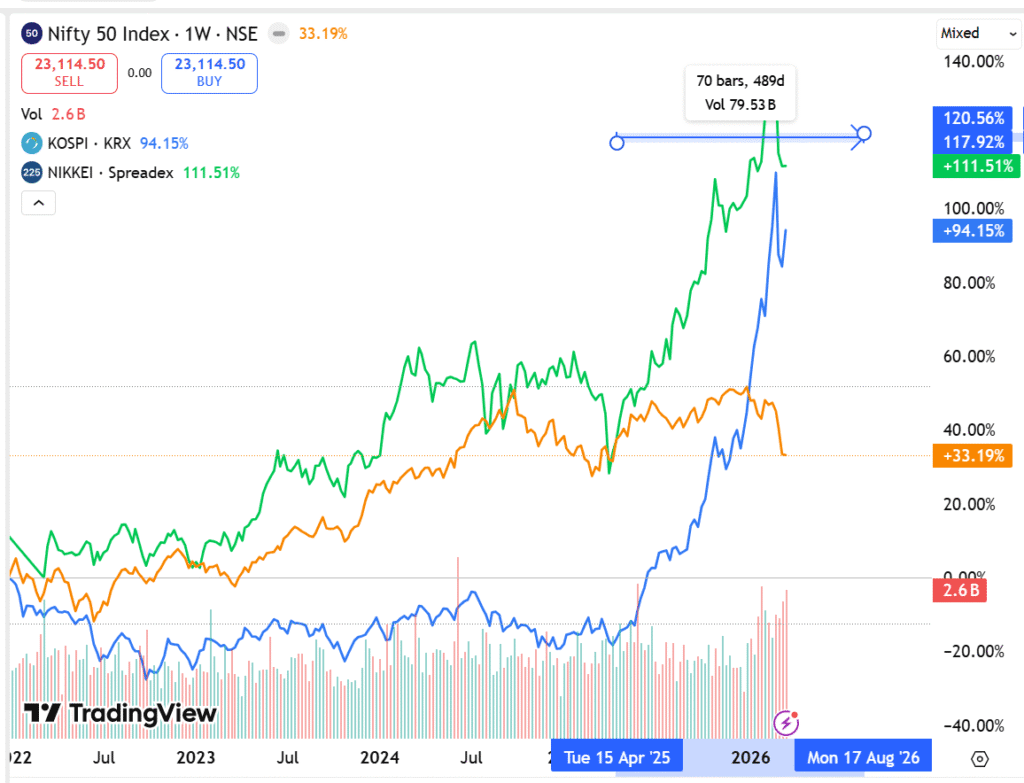

Simultaneously, global capital started rotating towards other emerging economies such as South Korea, Japan, China, and Hong Kong, where valuations were more attractive and growth narratives were improving. Government stimulus measures, advancements in AI, and a revival in manufacturing activity made these markets more appealing. As a result, FII outflows from India intensified through 2025 and into 2026. If we compare performance between April 2025 and March 2026, indices like KOSPI and Nikkei delivered significantly higher returns, nearly three times that of Nifty, while India saw a sharper correction of 15–20% compared to a relatively milder 5–10% correction in other emerging markets.

Impact of war:

The macroeconomic environment has further worsened the situation. The escalation of geopolitical tensions, particularly the Iran–Israel conflict, has led to rising crude oil prices, which in turn has fueled inflationary pressures globally.

A stronger US dollar has caused depreciation in emerging market currencies like the Indian rupee, making India less attractive for foreign investors.

This has resulted in persistent FII selling and heightened volatility in the markets. The impact of higher inflation is expected to reflect in upcoming quarterly earnings, suggesting that any recovery is likely to be gradual rather than immediate.

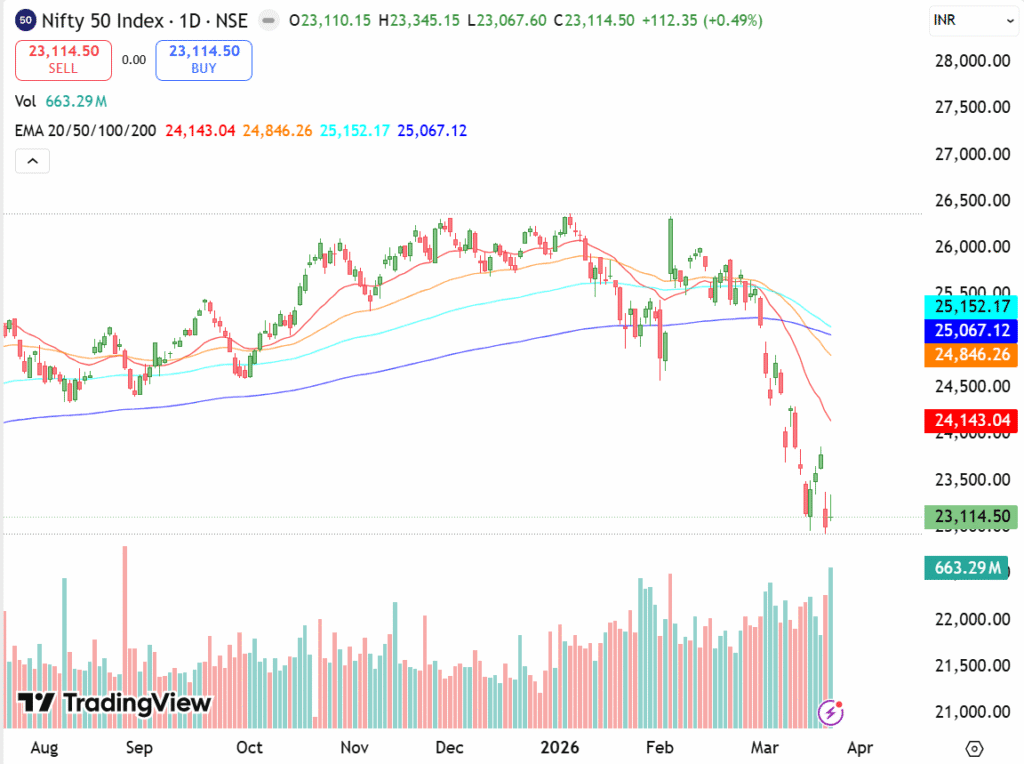

From a technical perspective, Nifty’s structure also indicates weakness. On the weekly chart, the index has been facing resistance near the 26,000 zone while attempting to hold support around 21,900 levels. It has already broken below its 100-week moving average and appears to be gravitating towards its 200-week moving average, which lies close to 21,900. On the daily chart, Nifty continues to trade below all its key moving averages, indicating a lack of strength and absence of a confirmed bottom.

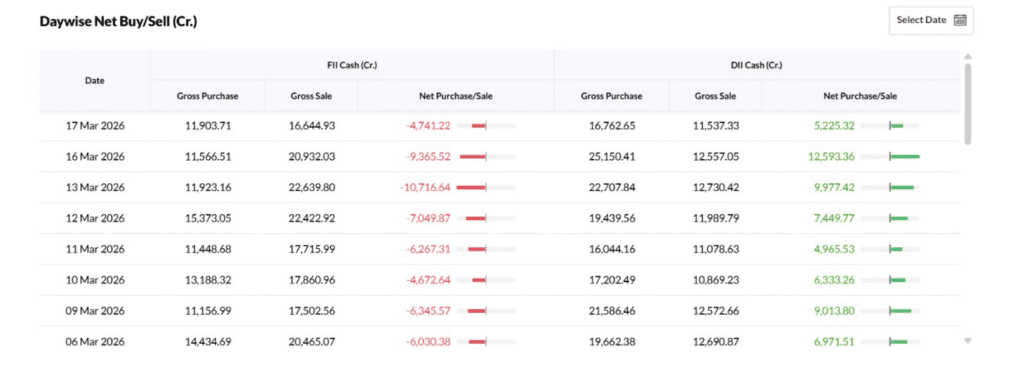

In this environment, investors should remain cautious. Rather than aggressively buying dips, the focus should be on waiting for clear signs of stability in the market. A sustained move above the 200-day moving average, supported by strong volumes and accompanied by a return of FII inflows (Currently the FII outflow looks outrageous as can be seen from the data table attached below), would provide better confirmation of a potential trend reversal. Until then, the market is likely to remain volatile, with recovery dependent on both earnings visibility and improvement in global macro conditions.

Overall, the current correction is not merely a technical pullback but a combination of valuation reset, global capital reallocation, and macroeconomic pressures. While India’s long-term growth story remains intact, the near-term outlook suggests that markets may first stabilize before embarking on a sustained recovery.