When the first missiles struck Tehran on the night of February 28, 2026, financial markets across the world were forced to reprice risk at a scale not witnessed since the Russia-Ukraine war of 2022. For India, a nation structurally exposed through its dependence on imported crude oil, the consequences were swift, deep, and are far from resolved. In this blog, we walk through the full arc of the conflict, assess its cascading impact on Indian equities, and explain why we remain cautious even as a fragile ceasefire takes shape.

Here’s what happened

Feb 28

Operation Epic Fury Launched

At 06:35 UTC, CENTCOM announced the commencement of joint US-Israeli strikes on Iran. Israeli Air Force executed decapitation strikes, Supreme Leader Ali Khamenei and several senior officials were killed in the opening hours. Iran immediately shut the Strait of Hormuz to tanker traffic.

Mar 1–5

Iranian Retaliation; Indian Markets Open in Shock

Iran launched over 550 ballistic missiles and 1,000+ drones at Israel and US bases in Bahrain, Kuwait, Qatar, Saudi Arabia, and the UAE. Dubai International Airport was struck and temporarily closed. Indian markets opened March 2 to a bloodbath, Sensex fell over 1,000 points in a session; ₹11 lakh crore wiped from market cap. Brent crude surged from $70 to above $80 within days.

Mar 10–17

Oil Crosses $100; Market Sell-Off Deepens

Brent crude pushed toward $97–100/barrel. Nifty 50 fell more than 10% in March, its worst monthly performance since March 2020. FIIs pulled out over $12 billion (₹50,000+ crore), the worst monthly sell-off on record. The rupee hit record lows near ₹92/$. Iran’s missile strikes declined sharply after day 10 as US-Israel strikes suppressed 75%+ of Iran’s launch infrastructure.

Apr 8

Two-Week Ceasefire Agreed, Brokered by Pakistan

Iran confirmed acceptance. The Strait of Hormuz was announced to be reopening. Global markets surged on the news; crude fell sharply. Pakistan PM Shehbaz Sharif invited both parties to Islamabad for permanent settlement talks on April 10. Trump called it “a big day for World Peace.”

As of morning, over 400 tankers remain anchored in the Persian Gulf. Only three ships have transited since the ceasefire was announced. Iran’s IRGC has established new controlled corridors, seeking to retain operational gatekeeping authority over the waterway.

Apr 9–10

Ceasefire Immediately Tested

Israel launched its largest-ever strikes on Beirut — targeting Hezbollah — within hours of the ceasefire taking effect, claiming Lebanon was not part of the deal. Iran disputed this and threatened to close the Strait again. As of today (April 10), only a handful of ships have transited Hormuz. The ceasefire is fragile, and Islamabad talks are just beginning.

What happened on Wednesday (8th April)

On the evening of April 7, approximately 90 minutes before President Trump’s threatened deadline to destroy Iran’s power plants and bridges, a two-week ceasefire was announced — brokered by Pakistan’s Prime Minister Shehbaz Sharif. The deal hinged on Iran agreeing to reopen the Strait of Hormuz, through which approximately 20% of the world’s daily oil supply passes, in exchange for a pause in US-Israeli military strikes.

Markets reacted with immediate euphoria. Oil fell 13-16% on Wednesday. The S&P 500 futures rose over 2%. Indian markets gapped up sharply, with Gift Nifty surging over 1,100 points — a mechanical short-covering rally driven by FIIs who had held 83-85% short positions in index futures going into the session.

Friday April 10, US Vice President JD Vance is leading an American delegation — alongside Steve Witkoff and Jared Kushner — into direct talks with Iranian counterparts at the Serena Hotel in Islamabad. This is the highest-level direct engagement between the US and Iran since the 1979 revolution.

All eyes lay on Islamabad to see if all parties turn up because very recently Iran has reported that there is no Iranian delegation in Pakistan and no talks are taking place if Lebanon attacks don’t stop.

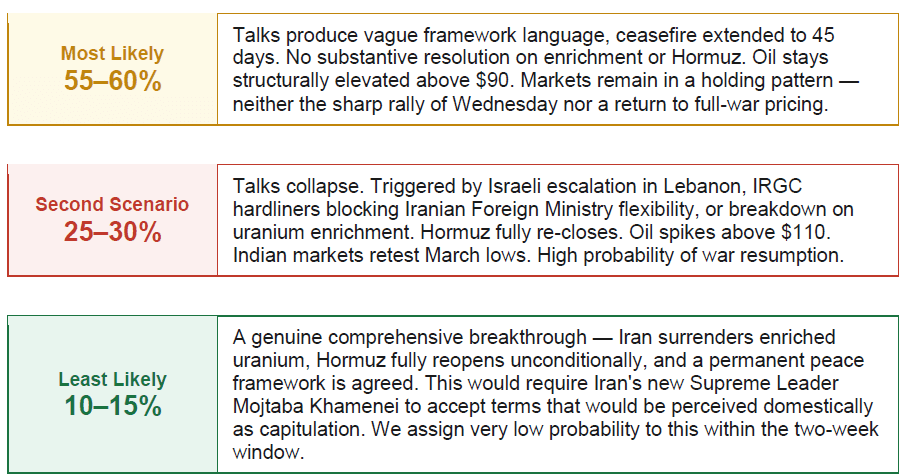

Our Outlook for Indian Equity Market (2026)

The core structural issue is this: the war has paradoxically strengthened Iran’s strategic leverage on Hormuz. Before February 28, closing the Strait was a threat. Now it is an established fact — Iran has demonstrated it can sustain the closure for six weeks under severe military bombardment. Iran will not voluntarily surrender that leverage in Islamabad.

We want to be direct with you: Wednesday’s rally was a short-covering event, not a fundamental shift. The four structural concerns we flagged in November 2025 — which drove our decision to reduce equity exposure well before the war began — remain entirely intact:

- AI Bubble Valuations — US mega-cap tech accounts for ~35% of the S&P 500. Debt-financed AI capex at historic levels. Any repricing cascades into Indian IT and global EM sentiment.

- Japan Carry Trade — Bank of Japan rate hikes continue to compress the yen carry, a multi-trillion dollar position funding global risk assets. The August 2025 unwind showed how violent this can be.

- Inverted Yield Curve — The US 10-2 yield spread continues to oscillate around inversion territory, historically one of the most reliable recession predictors with a 4–11 month lead time.

- High Inflation & Elevated Rates — Oil above $90 keeps India’s 10-year bond yield at 7.13% (a multi-year high). Goldman Sachs has pushed its first RBI rate cut call from June to September 2026. High rates compress equity valuations and slow earnings growth simultaneously.

The war accelerated the correction that was already in progress. A ceasefire removes one risk — and even then, incompletely — while leaving the other four structural concerns fully in place. We do not believe current levels offer an adequate margin of safety for long equity exposure.

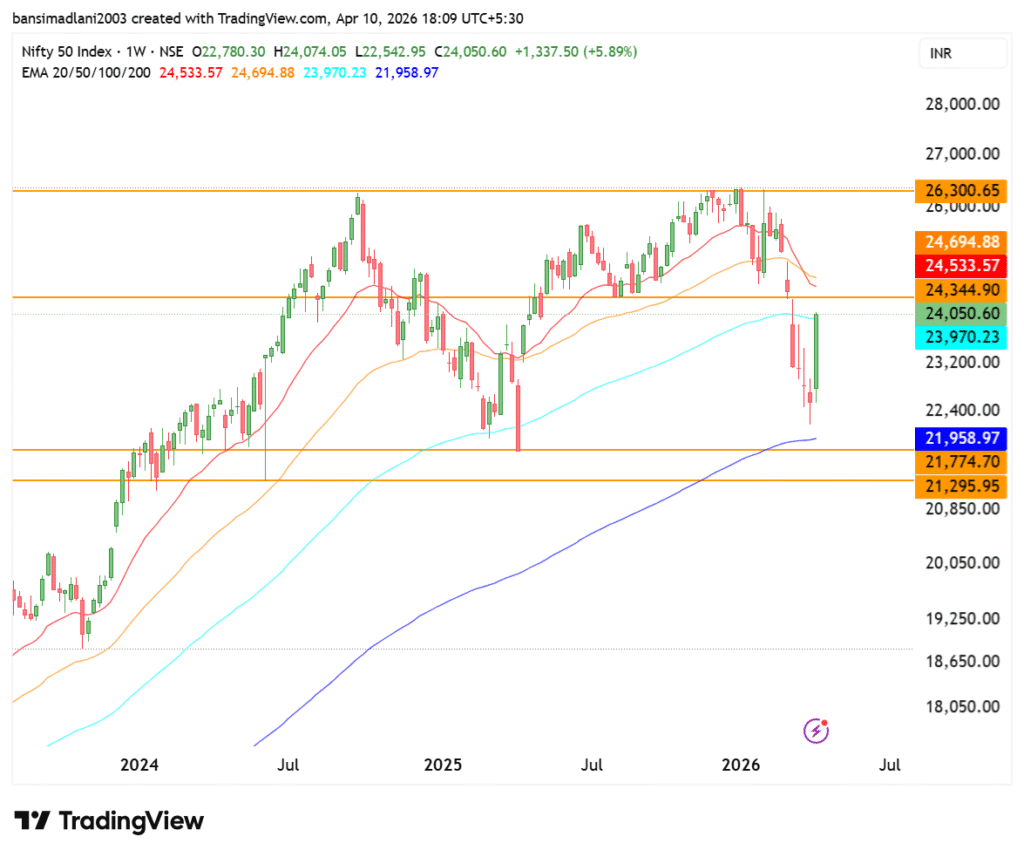

We expect Nifty to encounter strong resistance at the 24,000 level. Our recommendation remains: use any strength toward that level to further lighten equity positions. Remain overweight cash and short-duration, high-quality fixed income. We will revisit our stance when at least two of the four structural concerns show meaningful and durable resolution.

Over the next 72 hours we are watching, whether Vance and Iranian FM Araghchi actually sit in the same room and produce joint language out of Islamabad — or whether talks break down before they begin.