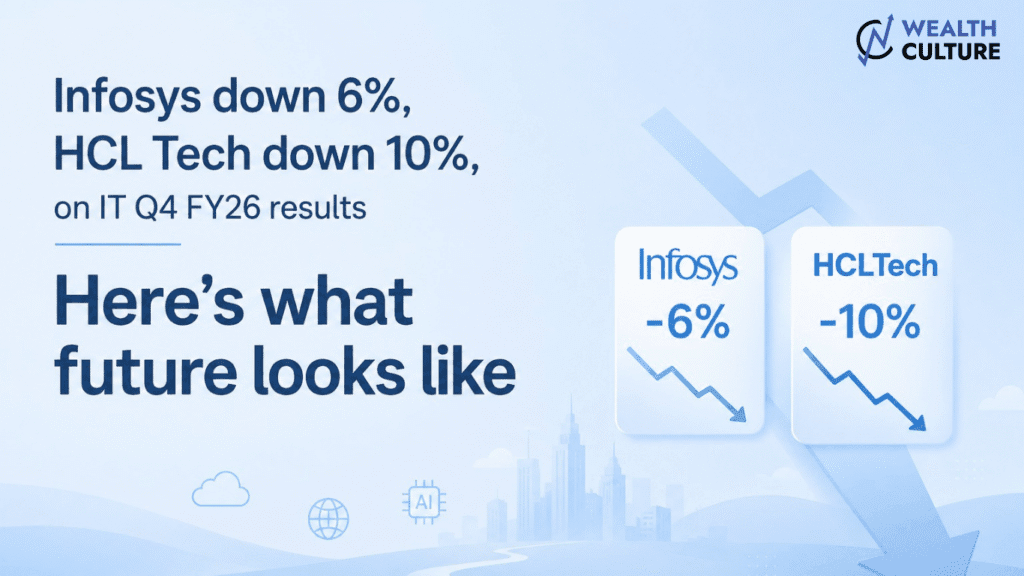

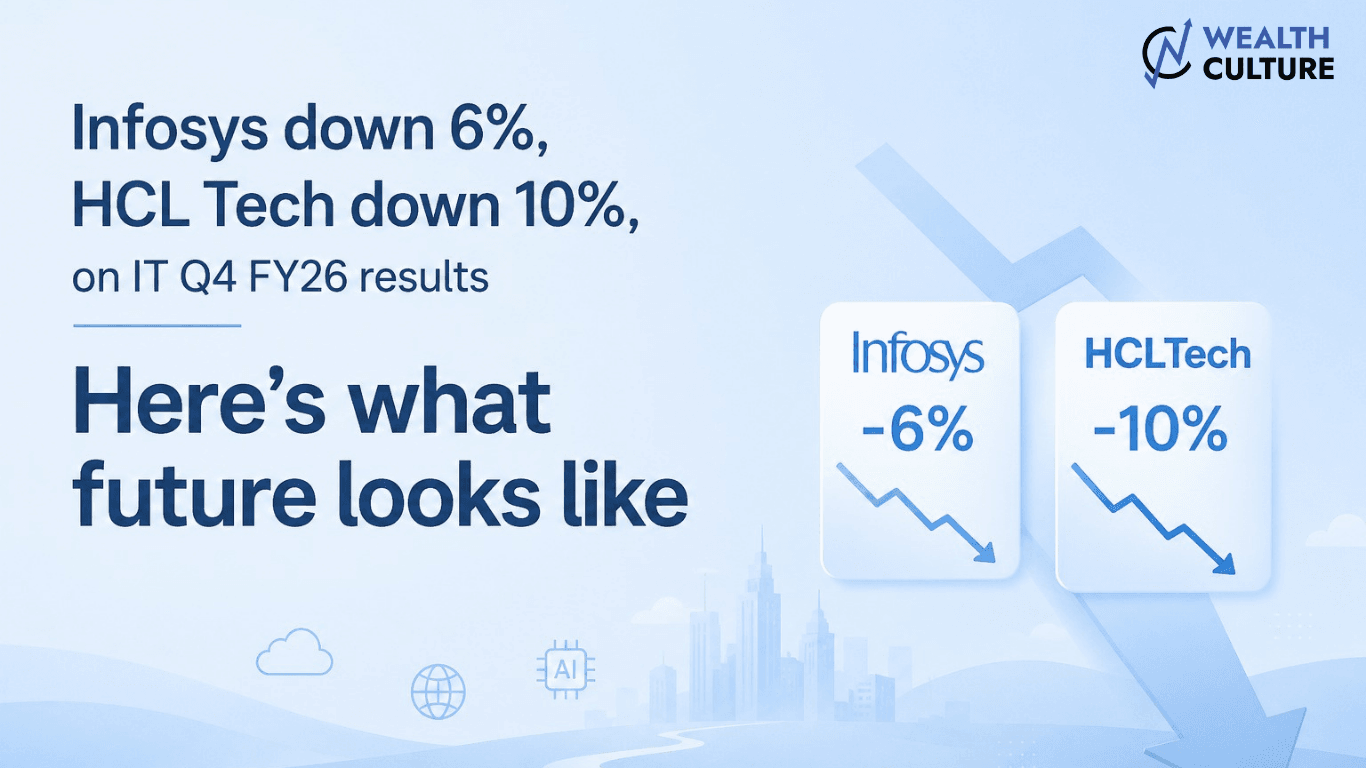

If there’s one thing FY26 results made clear, it’s that the Indian IT sector is no longer in its comfort zone. For years, the industry thrived on predictable growth, strong deal pipelines, and ever-expanding margins. But now growth is slowing, clients are hesitant, and AI — the biggest opportunity ahead — is ironically creating short-term pressure.

What we are witnessing is not a demand slowdown in the traditional sense. Companies continue to report strong pipelines and healthy deal wins. However, converting those deals into meaningful revenue is taking longer than expected. A big reason behind this is what many management teams subtly pointed out — AI-led productivity gains are being passed on to clients, reducing pricing power and compressing near-term revenues.

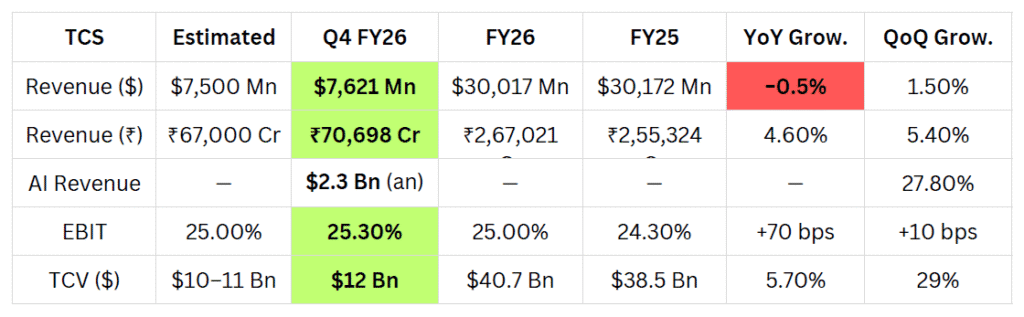

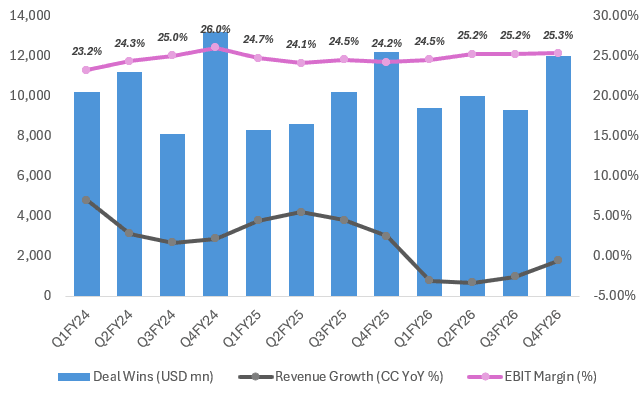

TCS: Stability Without Excitement

TCS delivered what can best be described as a stable but uninspiring quarter. Revenues remained largely flat on a year-on-year basis, and while margins saw a slight improvement, the overall growth momentum was missing. The interesting part, however, lies beneath the surface. The company reported AI-led revenues scaling to around $2.3 billion annualized, which signals that

Management commentary reflects a balanced tone — there is confidence in the medium-term pipeline, especially driven by GenAI-led transformation deals, but near-term visibility remains limited. BFSI, which is TCS’s largest vertical, continues to show cautious spending behavior, with clients focusing more on cost optimization and modernization rather than expansion. Healthcare, too, remains steady but not aggressive.

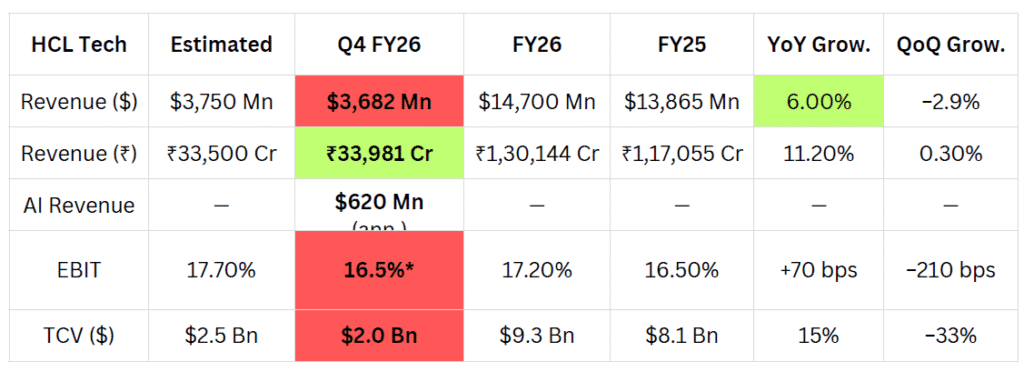

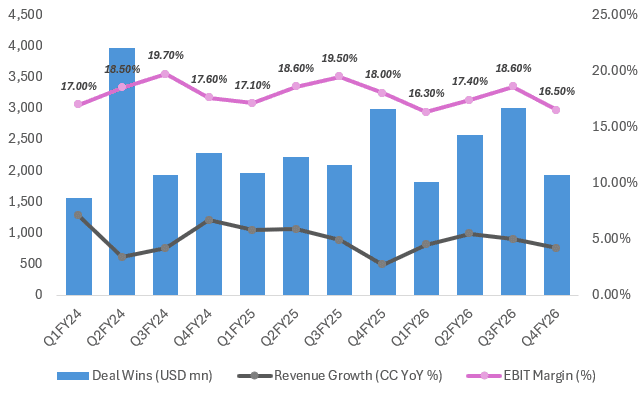

HCL Tech: Pressure Becoming Visible

HCL Tech’s performance highlights the cracks more clearly. While the company managed to deliver modest annual growth, the quarterly performance showed weakness, particularly in deal inflows.Telecom-led demand softness and continued delays in discretionary spending impacted overall momentum.

Management openly acknowledged that AI is starting to influence pricing, which is an important signal. The narrative is no longer just about AI driving growth — it is also about AI reducing billing intensity in the short term. Despite this, HCL remains relatively confident about maintaining margins through cost optimization and strategic acquisitions, which could add around 100–150 basis points over time. However, the growth guidance of roughly 1–4% for the coming year clearly indicates that the company is preparing for a subdued demand environment.

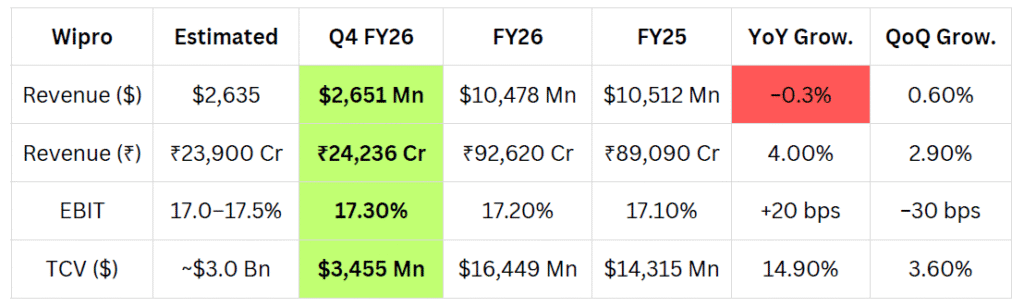

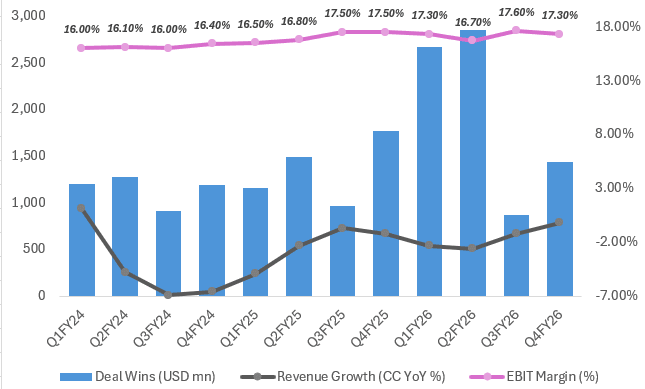

Wipro: Waiting for a Turnaround

Wipro’s results continue to reflect a company in transition. Revenues remained largely flat, and while margins held steady, there was little in the numbers to suggest a strong recovery ahead. The demand environment remains weak, especially in consulting-led programs, where discretionary spending has yet to pick up meaningfully.

Management commentary suggests that while deal pipelines are stable, conversion remains inconsistent. Regional performance also tells an interesting story — the Americas continue to struggle due to BFSI-related delays, while Europe shows some resilience, and APMEA is gradually gaining traction. The near-term guidance, which ranges between slight decline to marginal growth, reinforces the idea that Wipro is still in a wait-and-watch phase rather than an active growth cycle.

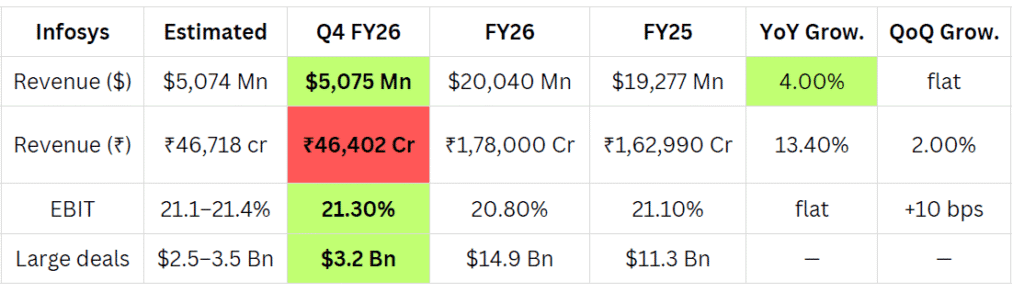

Infosys: Strong Deals, Slow Execution

Infosys presents a slightly more optimistic picture, but with a cautious tone. Clients are taking longer to finalize decisions, which delays revenue recognition.

Management highlighted steady but cautious demand, with delays in decision-making and discretionary spends, while AI-led deals and BFSI/energy verticals showed relative resilience.

Guidance remains conservative at 1.5%–3.5% CC growth for FY27 against expected range of 1.5-4.5%, reflecting macro uncertainty, slower deal conversions, and early-stage AI monetization despite a strong pipeline.

AI revenue remains at $275 million, contributing 5.5% of total revenue

Growth: Management describes it as “growing at a robust pace”, with AI now moving from pilots to scaled deployments across 90% of top client

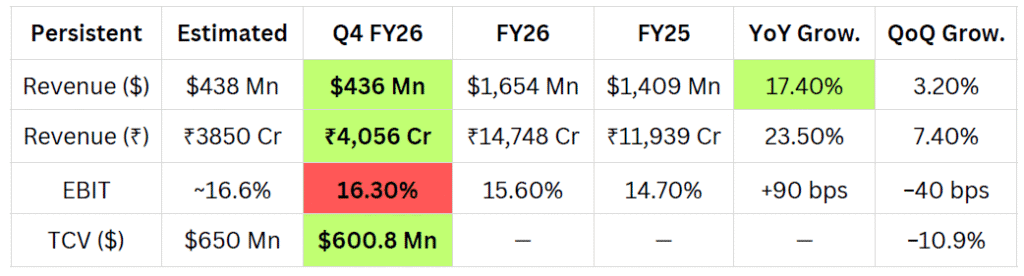

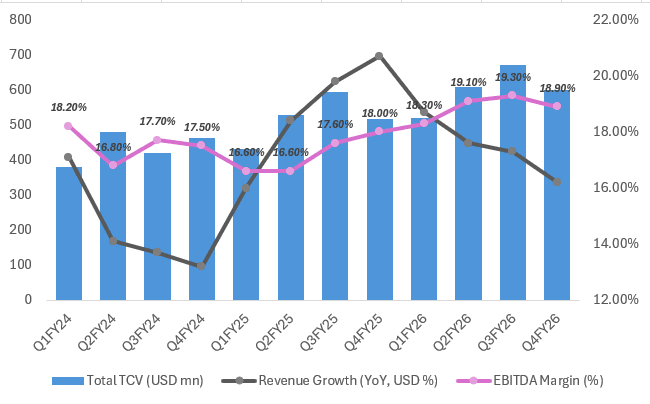

Persistent: The Quiet Winner

Amid all the caution surrounding large-cap IT, Persistent stands out as a clear outperformer. The company delivered strong double-digit growth, supported by robust AI-led platform traction and continued market share gains. Unlike larger peers, Persistent appears to be benefiting from agility — its ability to adapt quickly to emerging technologies and capture niche opportunities is translating into faster growth.

Profitability metrics also remain strong, with margin expansion driven by operational efficiencies and favorable deal mix.

Management remains confident on scaling, implying 15–17% CAGR required to reach~$5bn revenue by 2031, backed by AI, large deals, and continued market share gains(broadly consistent with current growth trajectory).

The Underlying Shift: AI is Reshaping the Model

One of the most important insights from this earnings season is that traditionally, IT services revenue was driven by billing hours and workforce scale but today, automation is reducing effort intensity, which directly impacts pricing.

This creates a paradox. Companies are closing more deals and building pipelines, but revenue growth remains muted because each deal is becoming more efficient. In simple terms, clients are delaying discretionary spending to adopt AI and reduce costs. It creates a short-term disconnect between demand and revenue growth.

What Comes Next?

In the near term, the outlook remains subdued. Discretionary spending is still delayed, BFSI continues to be soft, and companies are guiding for low single-digit growth. Margins are expected to remain stable, supported by cost control measures rather than strong revenue expansion.

The IT sector is going through a phase of adjustment. Forr investors and observers, the focus now needs to shift. Instead of just tracking revenue growth, the real indicators to watch are AI deal wins, conversion cycles, and the ability of companies to monetize new technologies effectively.